{kind=link}

Central Bank Digital Currencies and their Threat to Financial Freedom

Imagine you have an RM100 note in your pocket. You can use that to make any purchase, so long as the amount is within RM100. And the best thing is your purchases are confidential – or at least they are between you and the seller. You don’t have to worry about third parties knowing what you spend your money on, as it should be.

But what if your purchases, any purchase, can be traced and tracked? What if what you buy, what you pay for, isn’t private anymore? Such an assault on a fundamental freedom is one of the risks that comes with the advent of Central Bank Digital Currencies (CBDCs). International Business Review explores more.

In a world with so many different forms of digital currencies and payment systems such as cryptocurrencies, stablecoins and e-wallets, CBDCs may seem to be just another entry into an increasingly crowded field. One which, on the face of it, is supposed to make life easier on people by reducing, or even eliminating, their need to carry physical cash around.

However, what makes CBDCs stand out from the rest of the pack is the fact that they, unlike the others, are officially sanctioned and issued by national central banks. And because of this, CBDCs have the status of fiat currency. This makes them legal tender and gives them weightage that no other form of digital currency has.

Another key difference is that CBDCs are pegged to the currency of the issuing country at a 1 to 1 rate. Therefore, should Bank Negara Malaysia (BNM) issue its own CBDC, a single unit of that particular token will always be equivalent to RM1. This is unlike cryptocurrencies which are more volatile in valuation and may rise or fall depending on various market conditions.

This makes CBDCs similar to that of stablecoins, which are a form of digital currencies that are pegged to a fiat currency. However, while the value of stablecoins is pegged to fiat currency, they are not legal tender themselves. As such, merchants and vendors need not necessarily have to accept a stablecoin as a means of payment.

In addition, unlike cryptocurrencies which are decentralised, CBDCs are managed by a single authority, being the central bank that issues them. This means that any transaction or transfer of CBDCs needs to go through a centralised exchange, which is an important point that will come out later in this article.

The Rise of CBDCs

The events of the past three years, namely the COVID-19 pandemic have resulted in a surge in the popularity of digital payments, with more people avoiding handling physical cash – either as a matter of hygiene, health

and safety or just convenience.

For instance, according to McKinsey, between 2014 and 2021, the use of physical cash in Europe has gone down by one-third, with only 3 percent of transactions being made by cash in Norway.

Meanwhile, a report by HSBC reveals that, in Southeast Asia, Malaysia, Singapore, Thailand, Indonesia, the Philippines and Vietnam combined are expected to see the number of mobile wallets increase threefold to around 440 million by 2025. In Indonesia, for example, approximately 40 percent of all transactions are now done digitally.

In recent times, an increasing number of central banks around the world have indicated that they are looking at launching their own CBDCs, ostensibly to jump on the bandwagon and seize back the narrative of money, which has been seemingly overtaken in recent years by digitalisation, particularly cryptocurrencies.

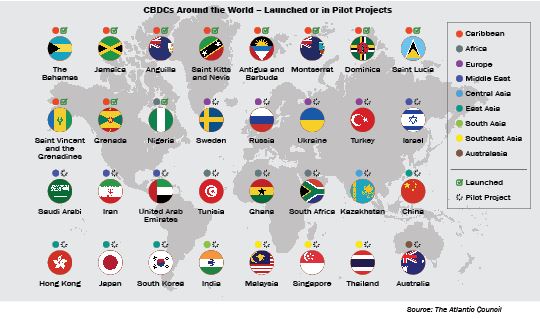

According to the US-based think tank the Atlantic Council, at present 11 countries have already launched CBDCs, while another 21 have started pilot projects, 32 are in the development stage, and 45 are in the research stage. For a full list of countries

that have either launched CBDCs or pilot projects, please refer to the table titled “CBDCs Around the World – Launched or in Pilot Projects”.

In Southeast Asia, Malaysia, Singapore and Thailand are in the pilot project stage of launching their own CBDCs, while Cambodia, Laos, Indonesia and the Philippines are in the midst of developing them, and Myanmar and Vietnam are still conducting research on them.

Malaysia’s own venture into CBDCs for instance started in June 2021, when BNM revealed that it was looking at having its own CBDC for cross-border wholesale payment settlement. This resulted in Malaysia joining Project Dunbar under the Bank of International Settlements (BIS), which is a project dedicated to exploring the use of digital currencies for international payments, co-led by BNM, the Monetary Authority of Singapore, the Reserve Bank of Australia and the South African Reserve Bank.

At the same time, BNM has also iterated that there are no plans to issue a CBDC for domestic retail trade. A sentiment which was repeated by then Governor Tan Sri Nor Shamsiah Mohd Yunus in 2022, and most recently in January 2023.

It is worth noting, however, that the BNM Governor did not dismiss the possibility of Malaysia having its own CBDC eventually, but that it does not presently see the need for one. Tan Sri Nor Shamsiah also revealed that BNM is “actively scaling up its internal capacity to support informed decisions on the CBDC” and that it would “look into the need of introducing a wholesale domestic CBDC before determining the need to issue a domestic retail CBDC”.

“Where an IRS breach puts all 331 million Americans at risk, a breach at a private financial institution would only affect a fraction of citizens – leaving customers at other banks free from harm.” – Norbert Michel, Vice President and Director, Center for Monetary and Financial Alternatives, Cato Institute and Nicholas Anthony, Policy Analyst, Center for Monetary and Financial Alternatives, in “The Risks of CBDCs” published by the Cato Institute

What are the Benefits?

With all that being said, what exactly are the benefits (if any) of CBDCs aside from central banks wanting to get in on an increasingly popular platform?

According to McKinsey, the adoption of CBDCs will allow financial services providers to save substantial costs, estimated at around US$400 billion annually, as they are able to save on spending on physical infrastructure.

In addition, CBDCs are also said to reduce the risks of fraud, financial crimes – such as money laundering – andcorruption as the authorities are able to keep track of each and every transaction along the way. This means that people cannot transact or transfer “dirty money” to one another without it leaving a (digital) paper trail.

CBDCs are also said to be useful in enhancing financial inclusiveness to those who are currently unbanked. According to the World Bank, approximately 1.4 billion people around the world in 2020 did not have any bank accounts. This effectively removed them from enjoying various services that a bank account provides, such as the ability to earn interest on savings. CBDCs could go some way into addressing this.

By programming a CBDC, money can be precisely targeted for what people can own and what people can do.”

– Bo Li,Deputy Managing Director, International Monetary Fund

The Dark Side of CBDCs

So, does this mean that we should go out right now and embrace CBDCs? Perhaps not. Because behind their veneer, CBDCs also hide some rather dark and disturbing aspects that should ring alarm bells in our heads.

For one thing, let’s address the biggest elephant in the room. Security. Since CBDCs are digital currencies, they are subject to the same cybersecurity risks as any other digital system.

In line with this, it is important to compare and contrast the differences between cryptocurrency networks and CBDC networks. Since the former is decentralised with different computers or servers being connected to one another without any central processor, taking one of the servers down will not affect the security of the transaction.

This is not the same for CBDCs, where everything goes through the central bank network. As such, an attack on that network could bring the system down and compromise the integrity of the entire nation’s financial and monetary network, thereby crippling the country. It will also have dire consequences on people’s financial security.

And let’s not forget about the issue which started this article. Financial privacy, or rather the lack of it. Because that is what CBDCs are threatening with the central bank’s ability to track and trace every transaction that is made.

This is made clear by Augustin Carstens, the General Manager of the Bank of International Settlements, who said. “We don’t know who’s using a US$100 bill today and we don’t know who’s using a 1,000 peso bill today. The key difference with the CBDC is the central bank will have absolute control on the rules and regulations that will determine the use of that expression of central bank liability, and also we will have the technology to enforce that.”

“Absolute control” is the key phrase here. Again, going back to the example given in the beginning, we are currently able to spend physical money without any limitation,so long as the price of the goods or services is equivalent to the valuation the merchant or vendor places on them.

CBDCs change the game entirely. Now, we increase the risks of government intervention into our spending habits. Sure, some people might say that it is a good thing because it means less opportunities for graft or for the purchase of dangerous or illegal items such as illicit drugs and firearms. However, it could also lead to the creation of, not a Nanny, but a Big Brother state, where you are limited in how you spend your own money.

Think that is far-fetched? Maybe not, especially when we consider this statement by Sir John Cunliffe, a Deputy Governor of the Bank of England, who described CBDCs in the following terms, “You could think of giving your children pocket money, but programming the money so that it couldn’t be used for sweets. There is a whole range of things that money could do, programmable money, which we cannot do with the current technology.”

Even today, certain governments have been overreaching and using their control of financial systems and networks to punish dissent. Take Canada for example, where the government in 2022 froze the bank accounts of Canadian citizens who donated to the Freedom Convoy – a group of truckers who were opposed to the COVID vaccine mandate. This was no doubt an assault on liberty, and to think that Canada is a so-called Western democracy.

Canadian truckers and their supporters during a Freedom Convoy protest against COVID-19 vaccine mandates which ruled that they would have to be vaccinated to cross the US border. The Trudeau government froze the bank accounts of people who donated to the truckers, thus leading to concerns over government overreach and how authorities can use CBDCs to lock people out of the financial system.

So, what happens if physical cash becomes a thing of the past and we all have to use CBDCs instead? Simply put, we will end up giving up so many fundamental freedoms. The freedom of privacy, the freedom of choice, the freedom to spend our own money on what we want. CBDCs may be the way of the future. But it is a dystopian future, and it is important that we oppose it at every step of the way.